Heading into 2026, regulatory, technological, and macro dynamics feel more aligned than they have been in years. Even amid persistent political noise, the transaction environment feels constructive and healthy. Acquirers and investors are euphoric, but they are constructive, engaged, and intentional in where they deploy capital. Where conviction is high, valuations have been strong. Where it is lower, many transactions are still getting done, often with more structure. From our perspective, this is the healthiest setup we’ve seen in years, and it positions 2026 to be an unusually active and productive year for Health IT transactions – and healthcare transformation.

Regulation is increasingly segmenting between value-based and consumer markets. The healthcare regulatory agenda is increasingly bifurcated between institutional value-based care and consumer-directed health. On the institutional side, Medicare Advantage Stars pressure, CMS value-based care expansion, and Medicaid redeterminations are driving sustained investment in data and infrastructure. On the consumer side, ICHRA expansion, broader HSA eligibility, and price transparency mandates are shifting purchasing power toward individuals and employers. The result is two parallel investment theses: platforms that support institutional risk-bearing models, and tools that help consumers navigate a more exposed purchasing environment.

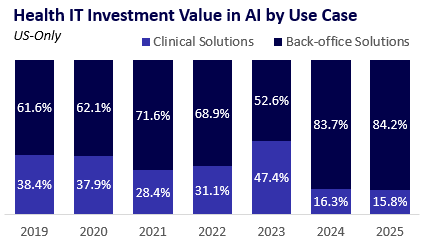

So far, AI is proving additive, not existential, for incumbents. While startup formation and funding remain active, incumbent Health IT platforms are also making meaningful AI investments within existing products. With access to proprietary data, established customer relationships, and embedded workflows, incumbents appear to face a manageable transition risk in this phase of AI adoption and, in some settings, may hold a structural advantage.

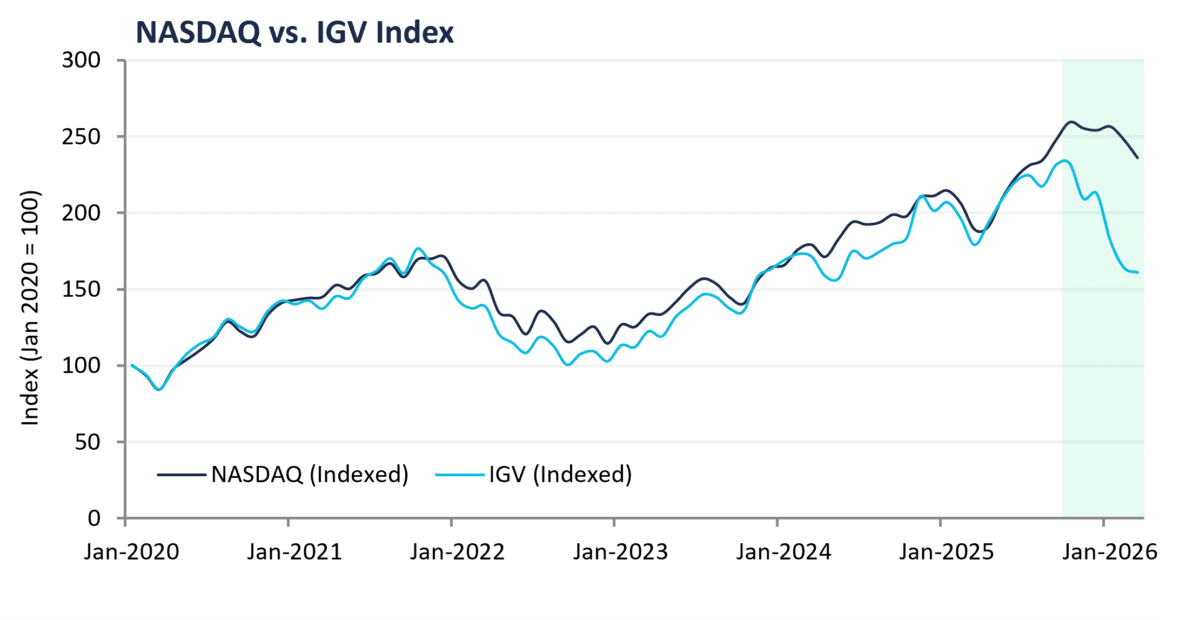

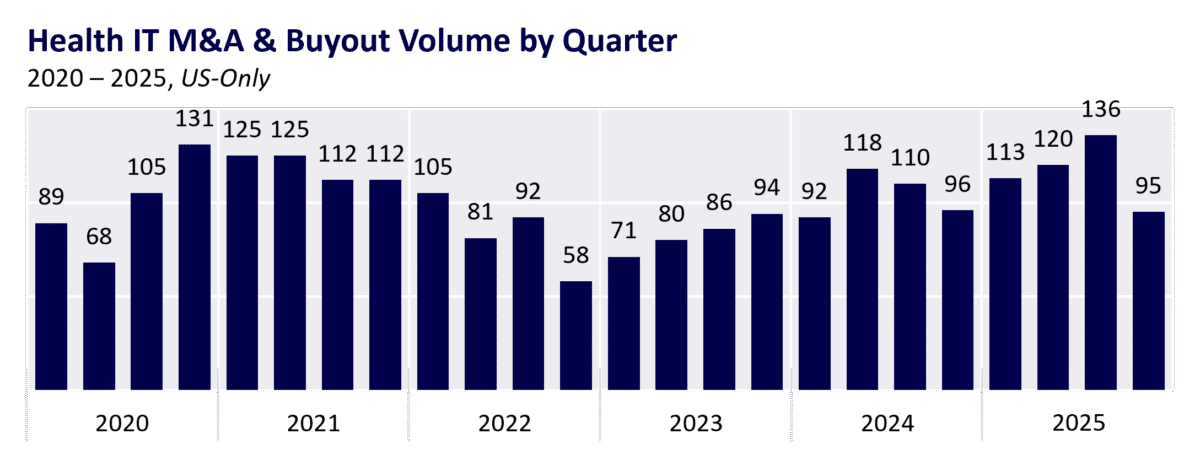

Health IT deal activity rebounded strongly in 2025. Growth equity recovered sharply, M&A activity reached all-time highs, and buyout volume, while modestly below 2024, remained near historical peaks. Valuations trended above pre-COVID levels, particularly for high-quality assets. Notably, quarterly M&A volume averaged 116 deals, a meaningful uptick from the 90 quarterly average in the period from 2022 – 2024.

Macro conditions have improved meaningfully. Inflation has moderated to roughly 2.6%, the Fed Funds rate has declined from the 5.25–5.50% range to 3.50–3.75%, and economic growth has remained resilient, with GDP expanding at 4.3% in Q3 2025 and forecasts calling for anywhere between 2-5% growth in Q4 (adjusted for the shutdown). Capital markets are functioning again, and the cost of capital is no longer the primary constraint it was just a few years ago.