2026 kicked off with considerable optimism and what felt like the healthiest setup for Health IT transactions in years. Reality has proven more challenging, shaped largely by two forces – the “SaaSpocalypse” and macro pressure tied to the Iranian conflict. Despite a challenging narrative, HGP’s firsthand experience has remained notably stronger than headlines would suggest, a perspective that appears supported by relatively resilient transaction activity.

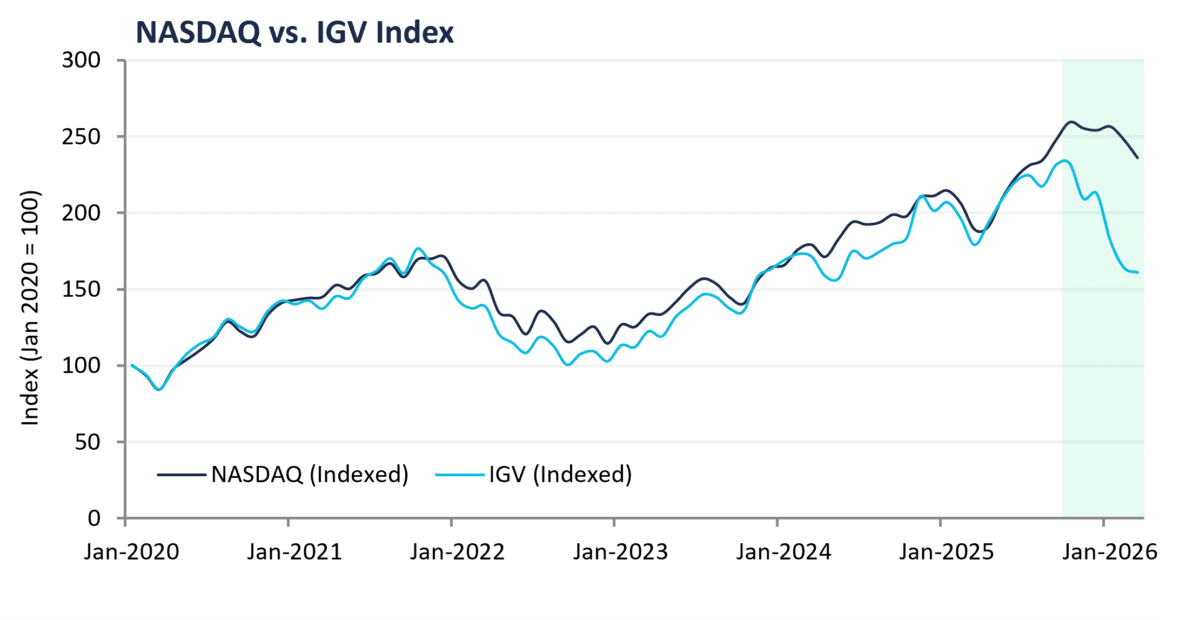

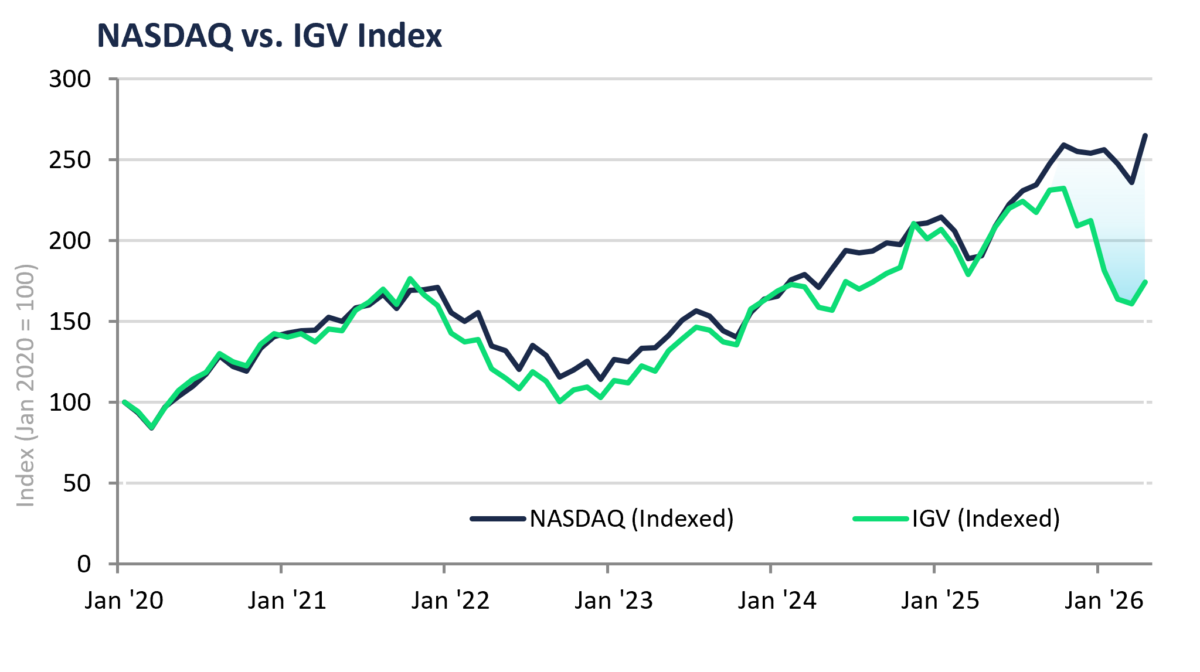

The “SaaSpocalypse” has emerged as a central narrative, reflecting the threat AI poses to incumbent enterprise SaaS companies. Public markets have reacted sharply. The HGP Enterprise SaaS Index has traded down from approximately 5.5x revenue in 2025 to 3.5x revenue in 2026. Private equity activity is mixed. Some investors are leaning in, while others are sitting on the sidelines waiting for greater clarity. Where private equity is active, it is generally underwriting to the view that the selloff is overdone, particularly for businesses with durable workflow embedment, strong retention, and clear paths to incorporating AI into their offerings.

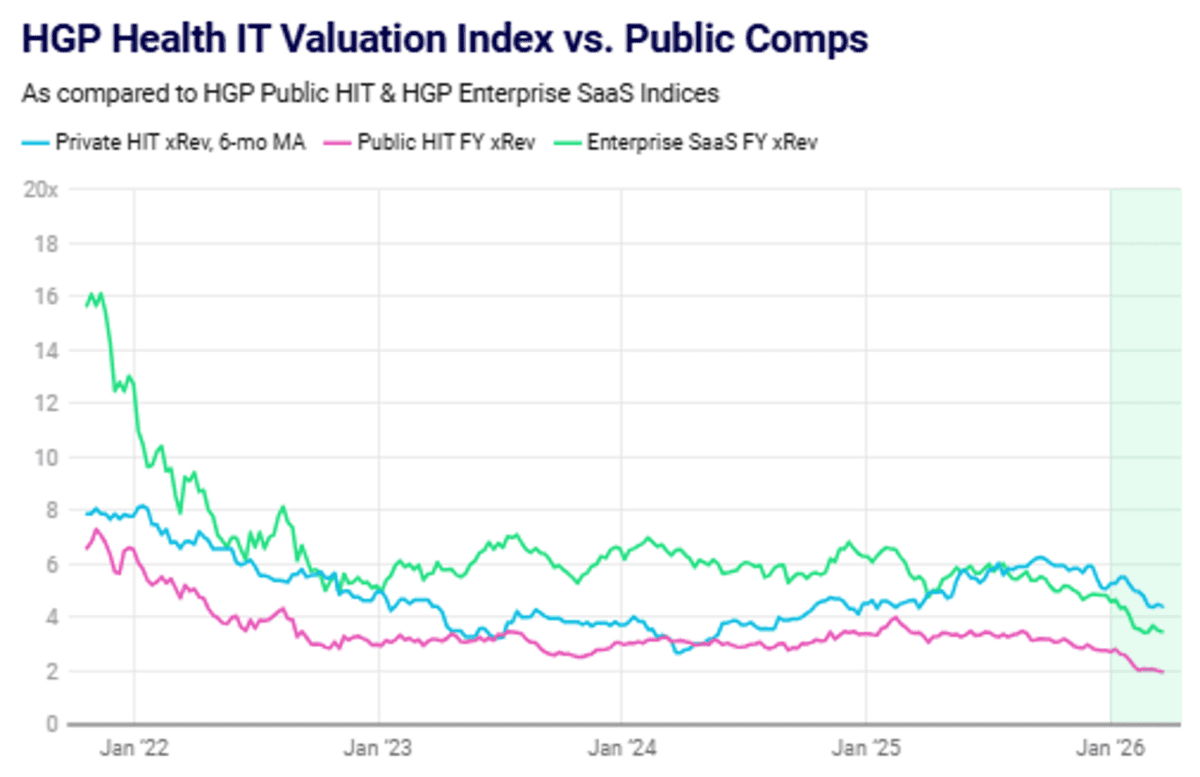

For the first time, the HGP Health IT Index is trading at a premium to the Enterprise SaaS Index, averaging approximately a 1x revenue premium. We attribute this to two factors. First, private market valuations do not move in lockstep with public markets and tend to be more stable through periods of volatility. More importantly, the healthcare market appears to favor system-of-record vendors in the context of AI. This reflects large volumes of unstructured data, meaningful privacy and compliance barriers, and deep integration within clinical and administrative workflows. Taken together, these dynamics may make it easier for incumbents to evolve into AI-enabled platforms than for AI-native entrants to displace them. The key question is how and if this gap resolves – does Health IT compress, or does Enterprise SaaS recover?

The other major market force is macro pressure tied to the Iranian conflict. Higher oil prices are feeding directly into inflation expectations, which in turn is keeping interest rates higher for longer. As a result, expectations for rate cuts have shifted meaningfully. At the beginning of the year, market-implied expectations (per CME FedWatch) pointed to approximately 3–4 rate cuts. That has now reset to a 50% chance that rates remain flat by year-end.

Both dynamics are also impacting private credit markets, a key funding source for dealmaking. Higher base rates, wider spreads, and a more cautious underwriting environment have created friction for transactions.

While the Iranian conflict has the potential to resolve relatively quickly, the SaaSpocalypse narrative is likely to play out over a longer period. The core question is whether the long tail of SaaS profitability remains durable through this cycle. Until there is greater clarity on that question, the enterprise SaaS market is likely to remain unsettled.

On the other hand, HGP’s firsthand experience tells a very different story. Our activity has remained strong, and equally important, we are seeing a healthy level of inbound interest from both buyers and sellers. Absent the broader market signals, our experience would suggest a very strong environment.

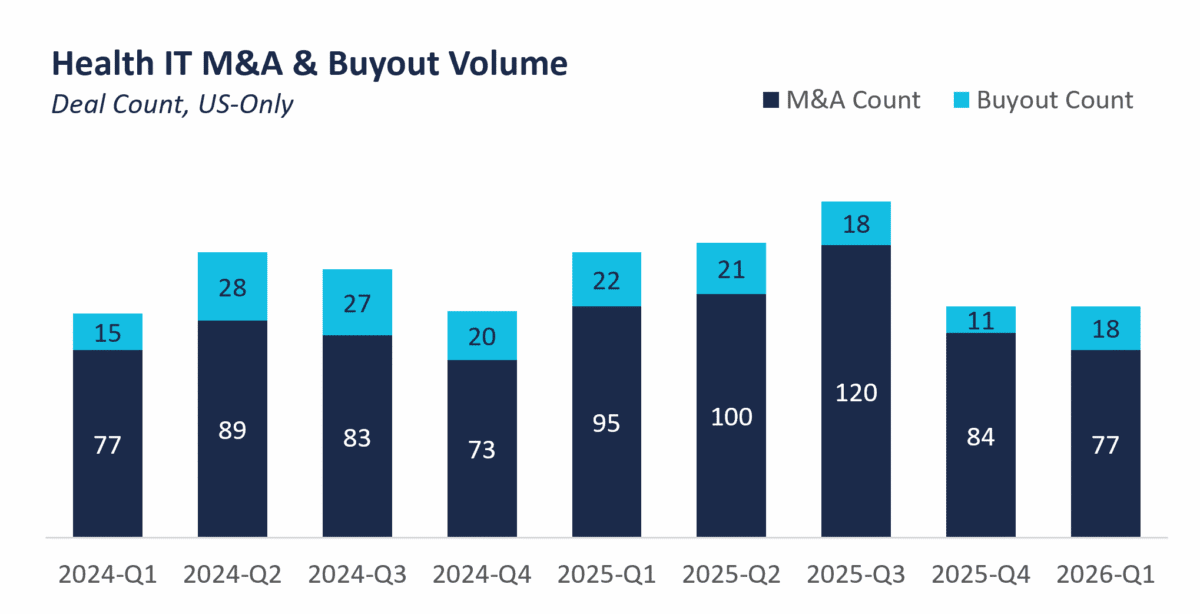

The data highlights a more nuanced story than headlines suggest, more in line with HGP’s experience. Q1 2026 recorded 95 Health IT M&A and Buyout transactions. While short of expectations, that level of activity points to a stable market, rather than one experiencing a meaningful slowdown. Notably, the quarter saw 18 high-quality buyouts, putting 2026 on pace to approximate 2025 levels, which marked the second-highest year for buyouts. Market caution appears to be impacting the upper end of the market, while the lower end has remained comparatively resilient.

Private equity sentiment is cyclical but not always right. The industry is highly benchmarked, which drives a herd mentality. Capital tends to be deployed when others are deploying and pulled back when others are pulling back. The post-COVID valuation environment is a clear example of how that dynamic can overshoot, and similar dynamics appear to be influencing how the market is currently pricing the disruptive risk of AI to incumbent enterprise SaaS. Much of the focus is on disruption – disintermediation, automation, and margin compression – which is easier to underwrite and visualize, while the potential for incumbents to expand is less appreciated. There is a natural tendency to overweight visible losses and underweight gains that are harder to see. That said, market sentiment cannot be ignored. It ultimately drives and destroys value, and companies need to be responsive to it. In Health IT, incumbents are well positioned to use AI to take share by embedding more deeply into workflows and replacing labor with software. If that execution materializes, sentiment could flip quickly, with investors assigning a premium to incumbents that demonstrate the ability to expand market share and increase wallet share through AI.

HGP’s outlook is admittedly mixed. We believe the public enterprise SaaS markets have overreacted to AI risk, but that risk is not uniform, with some companies far more exposed than others. This will create both opportunities and vulnerabilities. At the same time, we believe AI will expand total addressable markets for software companies in a meaningful way. In healthcare specifically, the dynamics we discussed earlier favor incumbents that can leverage their existing advantages to capture that upside. However, those advantages are not permanent. Software alone does not make a company successful, particularly in a market as complex as healthcare. Success is driven by go-to-market, value proposition, pricing, and execution. Incumbents have already demonstrated the ability to execute at scale in this environment, while most AI-native entrants have not. In healthcare, that execution gap matters. Maintaining that edge will require incumbents to deploy AI effectively. Those that do can strengthen their position. Those that do not risk obsolescence.