Recent experience is a stark reminder that what goes up must come down. But how far down? Compared to a year ago, market sentiment feels much more positive. While SaaS valuations remain suppressed, terminal interest rates have been met and the economy has demonstrated surprising resilience. The threat of a recession, while not dispelled, feels significantly less imminent than this time last year, injecting a much-needed dose of confidence into the market. Our report delves into critical market trends, leveraging data and experience gleaned from our own journey, to help you piece together your own market mosaic.

To download the complete report, drop your name and email in the sign up form at the footer of this page or in the footer of www.hgp.com and a copy will be sent to you. As always, please let us know if you have any questions or comments.

Key Takeaways:

After hitting a Q4 2022 nadir, 2023 US Health IT M&A and Buyout volume rebounded to levels consistent with pre-COVID. The final quarter, with 84 transactions, marked a 50% surge compared to the Q4 2022, as headwinds from rising capital costs, broader macroeconomic concerns, a tech-specific valuation reset, and a more cautious approach by investors abated throughout 2023.

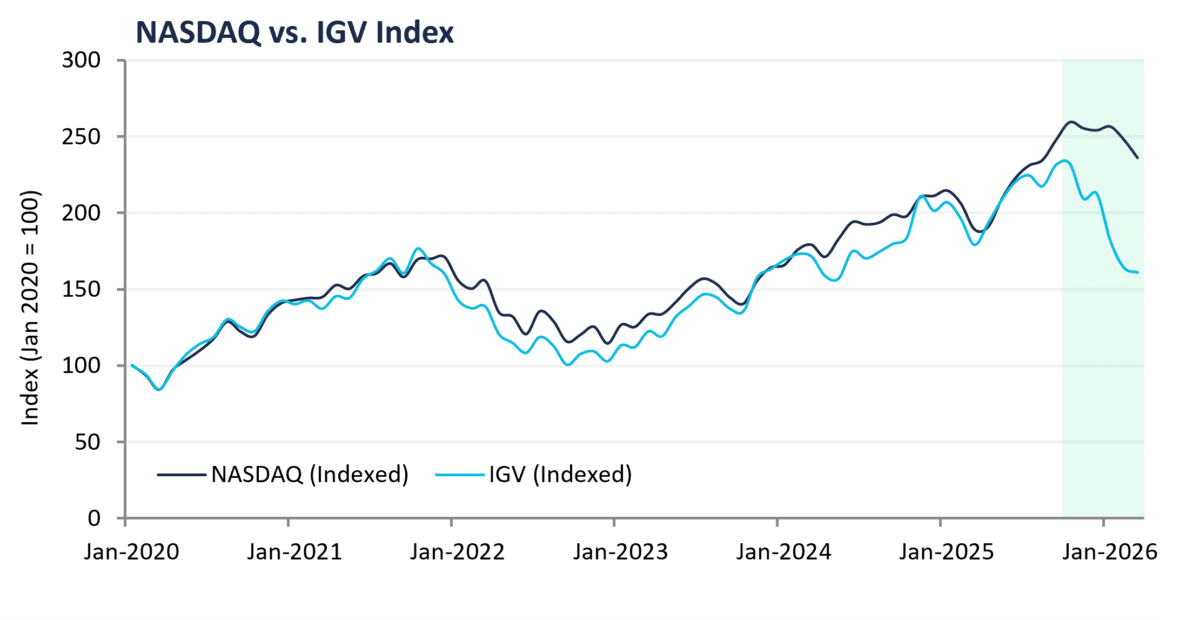

While deal volume returned to pre-pandemic norms, valuations languished particularly for revenue multiples. The HGP Enterprise SaaS Index closed 2023 at 7.6x revenue, 28% below its pre-COVID average of 10.5x. The HGP Health IT Transaction Index sank to 3.5x revenue, a near 30% discount from its pre-pandemic 4.6x average, a swing exacerbated by a lower quality mix of companies in the index. Despite this valuation gap, positive signals abound. Public equity markets and private investment data hint at an upswing in 2024.

The sentiment shift to profitability points to consistently strong EBITDA-based valuations, which have largely held steady from pre- to post-COVID in the 20-30x Forward EBITDA range (using the median of companies with <50x Forward EBITDA).

US Health IT investment activity fell to $9 billion in 2023 from $14 billion in 2022 and a record $29 billion in 2021, but modestly below the $11.5 billion pre-COVID average. Unlike M&A, which has been on the upswing through 2023, investment activity continued to fall through 2023, reaching a recent low watermark of 84 transactions in Q4 2023, a level not seen since Q1 2017.

The surge in new entrants, often targeting similar markets with overlapping offerings, led to market overcrowding leading to intensified competition, pricing dislocation, and challenges to scaling. While this has fostered innovation and new offerings, it has also created challenges for businesses to navigate, particularly in terms of achieving profitability and long-term success. Scalable, cost-effective, and AI-driven ventures are poised to capitalize on the current market vulnerabilities.

The number of publicly-traded Health IT companies contracted from 68 to 53 in the last two years. Of the remaining 53 constituents, 13 ended the year trading below or dangerously near $1, risking delisting due to noncompliance. Waystar is the only IPO in the queue, which is currently on-hold but likely to debut in 2024.

Core inflation has fallen to 3.9% but remains a stubborn distance from the 2% target. By the end of 2024, analysts project core CPI will fall to 2.4%. The Fed Funds rate stands at 5.25-5.5%. The FOMC dot plot implies a 4.5% rate by end of 2024, while futures markets project a 3.5-4.5% rate.