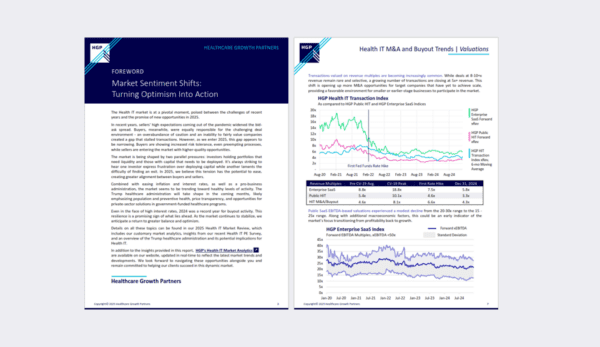

HGP Research & News

HGP research covers unique insights across the Health IT landscape, leveraging data and analysis from HGP’s proprietary Health IT transaction database.

HGP research covers unique insights across the Health IT landscape, leveraging data and analysis from HGP’s proprietary Health IT transaction database.